Close

Top Videos

Top Searches

Moods

Black Lives Matter

Chill

Christmas

Commute

Energy boosters

Feel-Good

Focus

Party

Pride

Romance

Sad

Sleep

Workout

Genres

African

Arabic

Blues

Bollywood & Indian

Christian & Gospel

Classical

Country and Americana

Dance and electronic

Decades

Family

Folk and acoustic

Hip-hop

Indie and alternative

J-Pop

Jazz

K-Pop

Latin

Mandopop & Cantopop

Metal

Pop

R&B and Soul

Reggae and Caribbean

Rock

Soundtracks and musicals

FRM: Swap rate versus spot rate

05:16

|

Download MP3

Related Videos

15:59

Option gamma (FRM T4-15)

6:18

FRM: Why we use log returns in finance

18:10

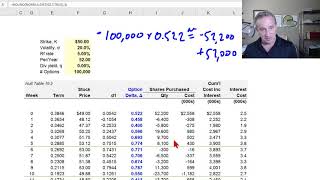

Option delta (FRM T4-13)

6:31

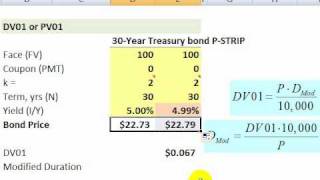

Bond DV01 and duration

19:59

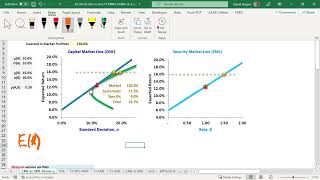

The SML is a general CML (informal FRM tip series)

15:21

Why par yields are the best interest rate measure

11:16

What is financial risk? FRM Foundations (T1-01)

9:20

FRM: Basis risk is the mother of all derivatives risk

19:46

Dynamic option delta hedge (FRM T4-14)

8:52

FRM: Forward rate agreement (FRA)

3:32

About our Bionic Turtle YouTube Channel (Trailer)

8:56

What is value at risk (VaR)? FRM T1-02

5:59

FRM: Intuition behind the Black-Scholes-Merton

8:42

Forward rates are implied by zero rates (FRM T3-11)

8:42

ABCs of CDO (CLO, CBO, CDO of ABS)

11:50

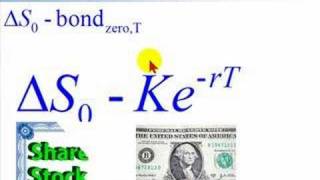

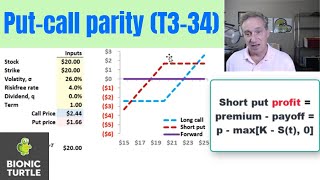

Put-call parity (T3-34)

7:36

FRM: Collateralized debt obligation (Balance Sheet CDO)

19:44

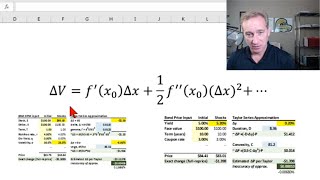

Delta-gamma value at risk (VaR) with the Taylor Series Approximation (FRM T4-4)

6:53

FRM: Binomial (one step) for option price

16:33

Fixed Income: Infer discount factors, spot, forwards and par rates from swap rate curve (FRM T4-25)

15:59 6:18 18:10 6:31 19:59 15:21 11:16 9:20 19:46 8:52 3:32 8:56 5:59 8:42 8:42 11:50 7:36 19:44 6:53 16:33

15:59 6:18 18:10 6:31 19:59 15:21 11:16 9:20 19:46 8:52 3:32 8:56 5:59 8:42 8:42 11:50 7:36 19:44 6:53 16:33